Meet the Offender: Loopholia, Inc.

Loopholia is the Beyoncé of tax planning — it does it all, flawlessly. Structured as a U.S.-based C corporation with 4 wholly owned subsidiaries, it operates across logistics, tech, manufacturing, and media, with a low-tax IP holding company based in Ireland.

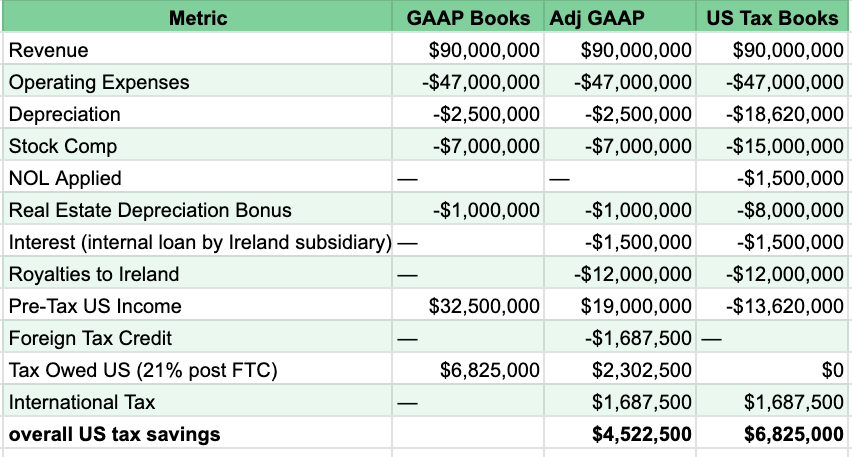

It earned $90 million this year and reported $34.5 million in GAAP (book) profit.

But after applying every strategy we’ve covered in The Write-Off Diaries, Loopholia’s taxable income falls to zero — and its federal income tax bill becomes $0.

Let’s break down exactly how they did it.

Loopholia’s 8-Step Corporate Tax Elimination Plan

Featuring side-by-side GAAP vs. tax books, internal loans, real estate plays, and a hair-flipping finale worthy of a stadium tour, this is corporate tax planning in full formation.

Each step includes:

- ✅ What they did

- 🧠 Why it works

- 📉 The book-vs-tax impact

- 💸 Total benefit to taxable income or tax owed

1. Bonus Depreciation & Section 179

What They Did:

Bought $15M in logistics equipment + $1.22M in tech upgrades.

Why It Works:

Thanks to 100% bonus depreciation under the One Big Beautiful Bill, they wrote off the entire $16.22M in 2025.

Book Depreciation: $1.5 million Tax Depreciation: $16.22 million

Net Additional Deduction: $14.72 million

2. Net Operating Loss (NOL) Carryforward

What They Did:

Used $10M in prior-year losses.

Why It Works:

NOLs can offset up to 80% of taxable income. Loopholia applied $8M this year.

Book: No effect Tax: ($8M) deduction

Net Additional Deduction: $8 million

3. R&D Tax Credit

What They Did:

Spent $2.5M developing an internal logistics algorithm.

Why It Works:

With a prior 3-year R&D average of $1.5M, the excess was $1.75M. They claimed 14% of that.

Credit = 14% × $1.75M = $245,000

GAAP: Expense part of P&L Tax: Credit against liability

💰 Direct Credit: $245K

4. Stock-Based Compensation

What They Did:

Issued stock options worth $7M at grant, exercised for $15M.

Why It Works:

GAAP records the $7M. IRS allows a $15M deduction when exercised.

Net Additional Deduction: $8 million

5. Transfer Pricing & Offshore IP

What They Did:

Moved their proprietary software to Ireland. Paid $12M in royalties to use it.

Why It Works:

U.S. entity deducts the $12M, while Irish subsidiary pays only 12.5% tax on it.

Book: Neutral Tax: ($12M) deduction

Net Additional Deduction: $12M

6. Internal Lending (Interest Deduction)

What They Did:

Irish IP company loans $25M to the U.S. parent. U.S. pays 6% interest ($1.5M/year).

Why It Works:

Interest is deductible in the U.S. and taxed lightly in Ireland.

Net additional Deduction: $1.5M

7. Real Estate Depreciation & 1031 Exchange

What They Did:

- Sold an old warehouse for $10M

- Bought a new $12M facility using a 1031 exchange

- Used cost segregation to front-load depreciation

Why It Works:

- 1031 = No capital gains recognized

- Cost seg boosts first-year deduction

Book Gain on Sale: $2.2 million Book Depreciation: $1 million

Tax Gain on Sale: $0. Tax Depreciation: $2.4 million

Net additional Deduction: Deferred Gain

$1.4 million. $2.2 million

FInal Result GAAP vs GAAP allowed Adjustments vs Books for US Tax purposes

But Wait — Let’s Talk Credits (and Carryforwards)

First: The R&D Tax Credit (Yes, It’s Real — Kinda)

We gave Loopholia a generous $600,000 R&D credit. But here’s the fine print:

- The R&D credit is non-refundable, meaning it can’t reduce taxes below zero.

- In this case, Loopholia already zeroed out its U.S. tax liability with deductions.

- So technically, that $600K credit doesn’t generate a refund — but it can be carried forward for up to 20 years.

- Exception: In certain cases (especially startups or qualified small businesses), the credit can offset payroll taxes, like the employer portion of FICA, and that can trigger a refundable benefit.

So no, it’s not Monopoly money. It’s just delayed Monopoly money — or a really awkward IOU that says: “Redeem next decade.”

Second: The Foreign Tax Credit Saves the Day

You’ll notice Loopholia didn’t pay U.S. taxes, but it did pay $1.687 million in foreign taxes (thanks, Ireland).

Enter the Foreign Tax Credit — a nifty little provision that lets companies subtract taxes paid abroad from what they owe the U.S.

- That $1.68M wiped out the U.S. tax liability of $2.3M shown under Adj GAAP.

- End result: Zero U.S. tax due, and everyone’s compliance officer gets a gold star.

And Don’t Forget: The NOL Carryforward (Now Even Juicier)

After all the deductions, credits, and strategic international shenanigans, Loopholia didn’t just reduce their U.S. tax bill — they reported a U.S. loss of $13.2 million on their tax books.

- That loss isn’t wasted — it becomes a Net Operating Loss (NOL).

- The IRS allows companies to carry forward NOLs indefinitely (post-TCJA), but only up to 80% of future taxable income per year.

- So Loopholia now has $13.2M in tax losses sitting on their balance sheet like a gift-wrapped tax deferral — ready to slash future liabilities.

This isn’t just tax planning — it’s tax pre-gaming.

Recap: The Credits, the Loss, the Legend

- R&D Credit: $600,000 non-refundable, carried forward

- Foreign Tax Credit: $1.687M, fully offsets U.S. liability

- NOL Carryforward: $13.2M ready to offset future earnings

Between the credits and the carryforward, Loopholia has built a tax bunker so deep the IRS would need a fiscal jackhammer to get through.

Final Receipt: The Write-Off Diaries in Review

After 10 deliciously infuriating parts, one thing should be clear: the tax code isn’t broken — it’s doing exactly what it was lobbied to do. From depreciation acrobatics and international profit limbo, to R&D write-offs for “trying your best,” this series has walked you through the buffet of legal levers that allow corporations to appear broke while swimming in profits. And we didn’t even need a Panama bank account to prove it. If you’ve ever wondered why the largest companies pay so little in taxes while your small business accountant tells you to save receipts for printer toner, well… welcome to the game. The real loophole isn’t just in the law — it’s in the language, the politics, and the public’s short attention span. But now that you’ve made it through The Write-Off Diaries, you’re fluent in corporate tax strategy — and maybe just cynical enough to do something about it.

.svg)